New England Economic Conditions Through January 14, 2025

Key Takeaways

- Inflation in New England continued to recede in November 2024, converging toward the national rate. Moderation in price appreciation across key expenditure categories—including shelter, transportation, medical care, recreation, and education—contributed to the overall cooling of inflation in the month.

- House-price and rent growth in New England steadily decelerated, with Vermont, Massachusetts, Maine, and New Hampshire experiencing more substantial slowdowns compared with Connecticut and Rhode Island.

- New England’s recent employment growth shifted toward the educational and health services, government, and leisure and hospitality sectors and away from the professional and business services, manufacturing, and information sectors. Because the sectors that experienced slower employment growth are high-productivity sectors, the change was associated with modestly slower GDP growth in the region.

Sign up for new research and data on the New England economy.

Payroll Employment

- New England’s recent employment growth shifted toward the educational and health services, government, and leisure and hospitality sectors and away from the professional and business services, manufacturing, and information, the sectors that drove employment growth in the pre-pandemic period.

- Because the sectors that experienced slower employment growth are high-productivity sectors, the change in the employment composition was associated with modestly slower GDP growth in the region.

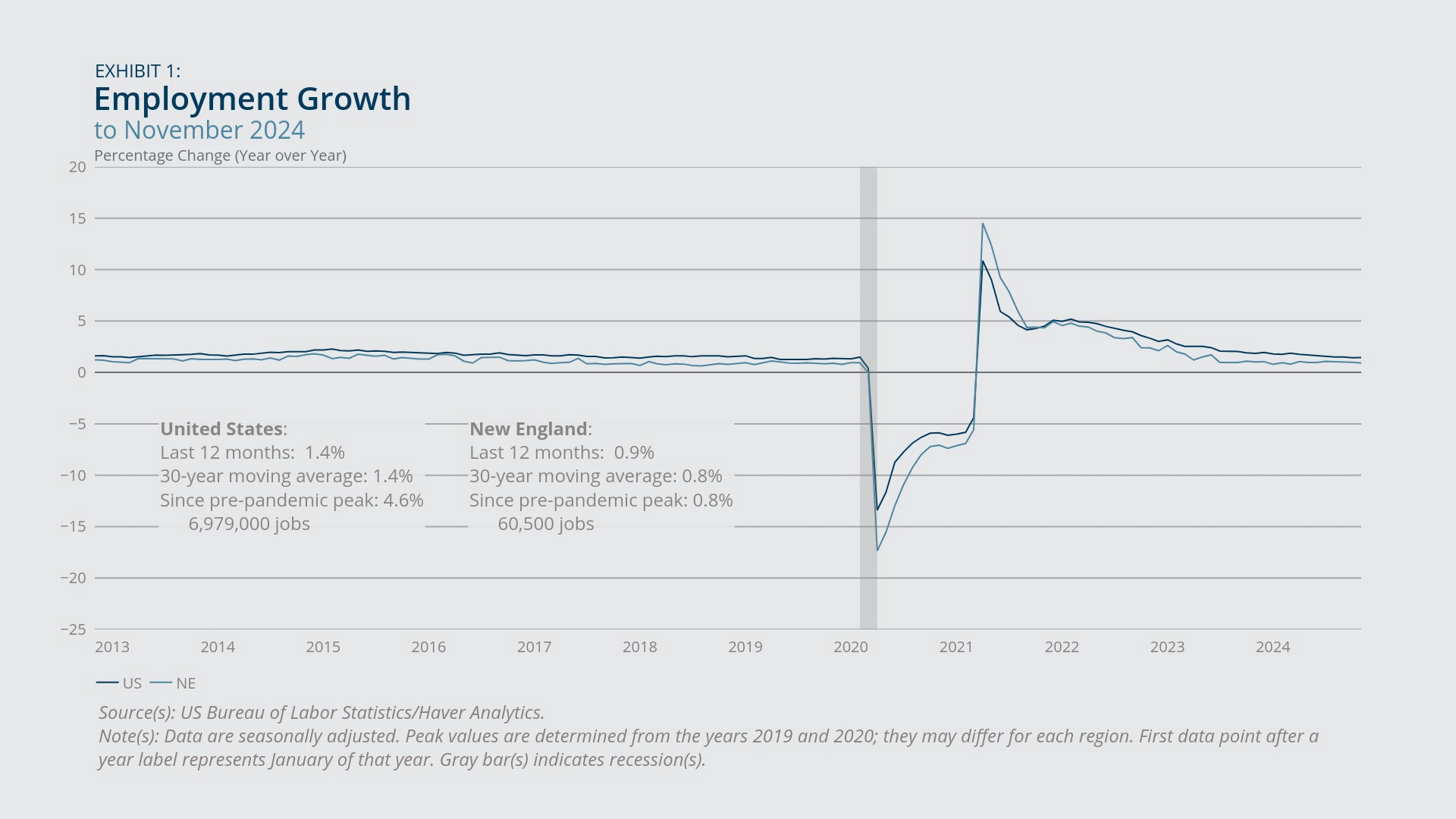

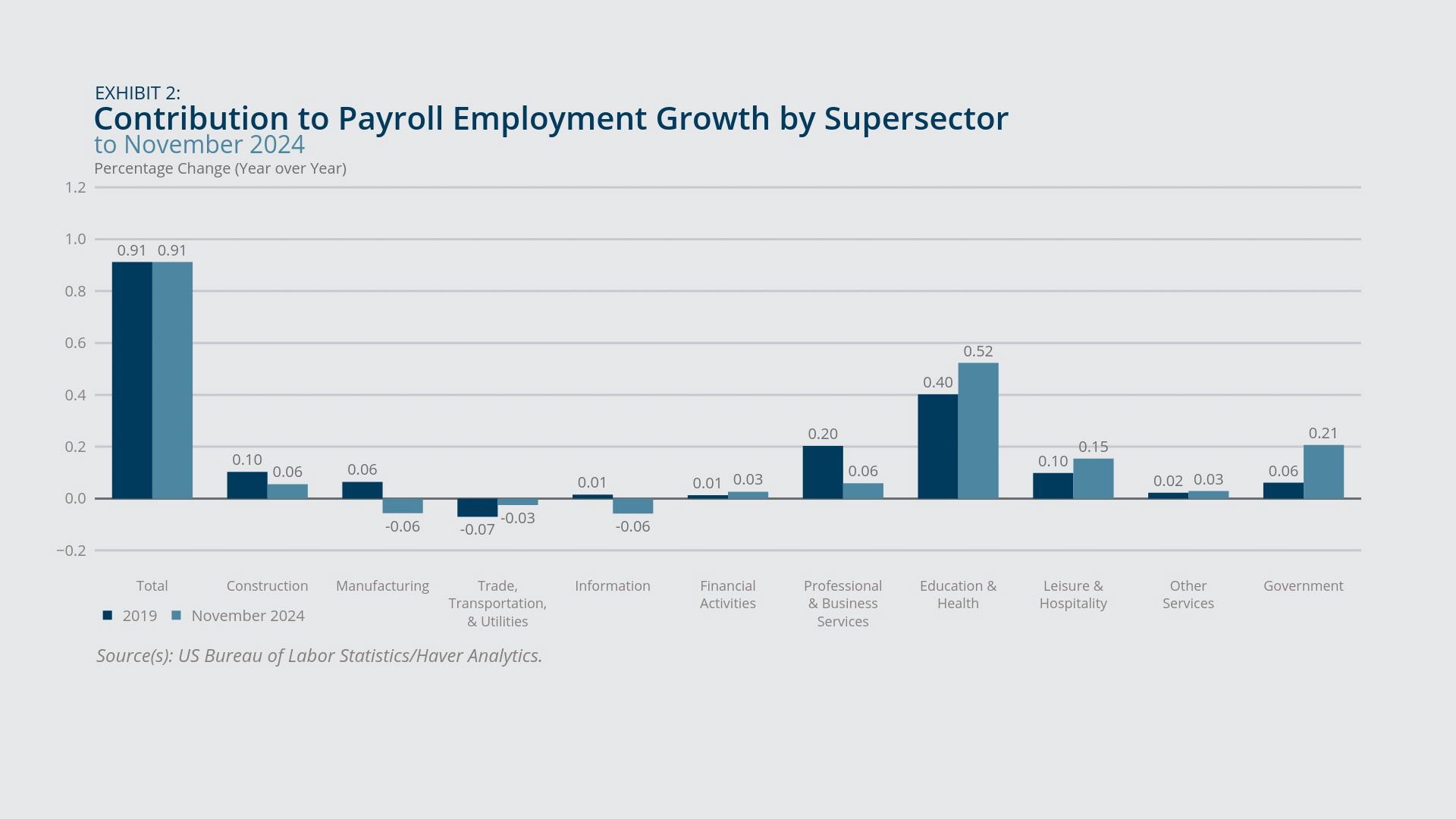

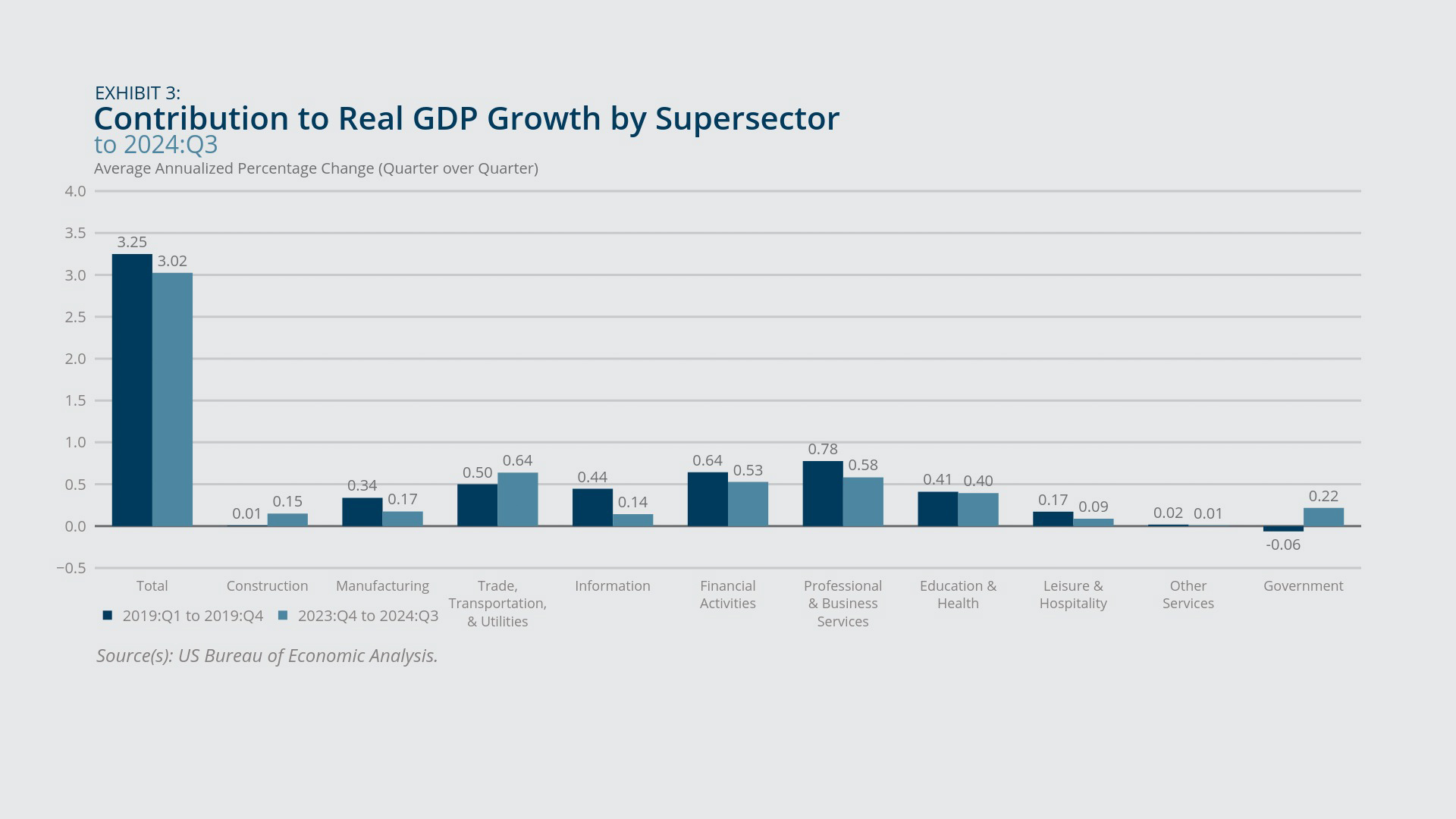

In November 2024, payroll employment in New England grew 0.9 percent year-over-year, which is on par with the average growth rate observed in 2019 (Exhibit 1), before the COVID-19 pandemic. The growth was driven primarily by the educational and health services, government, and leisure and hospitality sectors, which collectively accounted for more than 80 percent of the gross employment increase from November 2023 to November 2024 (Exhibit 2). The region’s recent employment growth shifted toward these three sectors and away from the business services, manufacturing, and information sectors. The shift in the employment-growth drivers is noteworthy because the declining sectors, on average, have higher output per worker than the growing sectors. Consequently, the change in the employment composition was associated with a modest deceleration of the region’s total real GDP growth, despite the observed relatively strong employment growth and improved productivity (Exhibit 3).

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Unemployment and Labor Force Participation

- While the national unemployment rate increased steadily over the 12-month period ending in November 2024, New England’s unemployment rate remained close to 3.5 percent.

- Labor market resilience was observed across the region, as each New England state experienced growth in the employment-to-population ratio during this period.

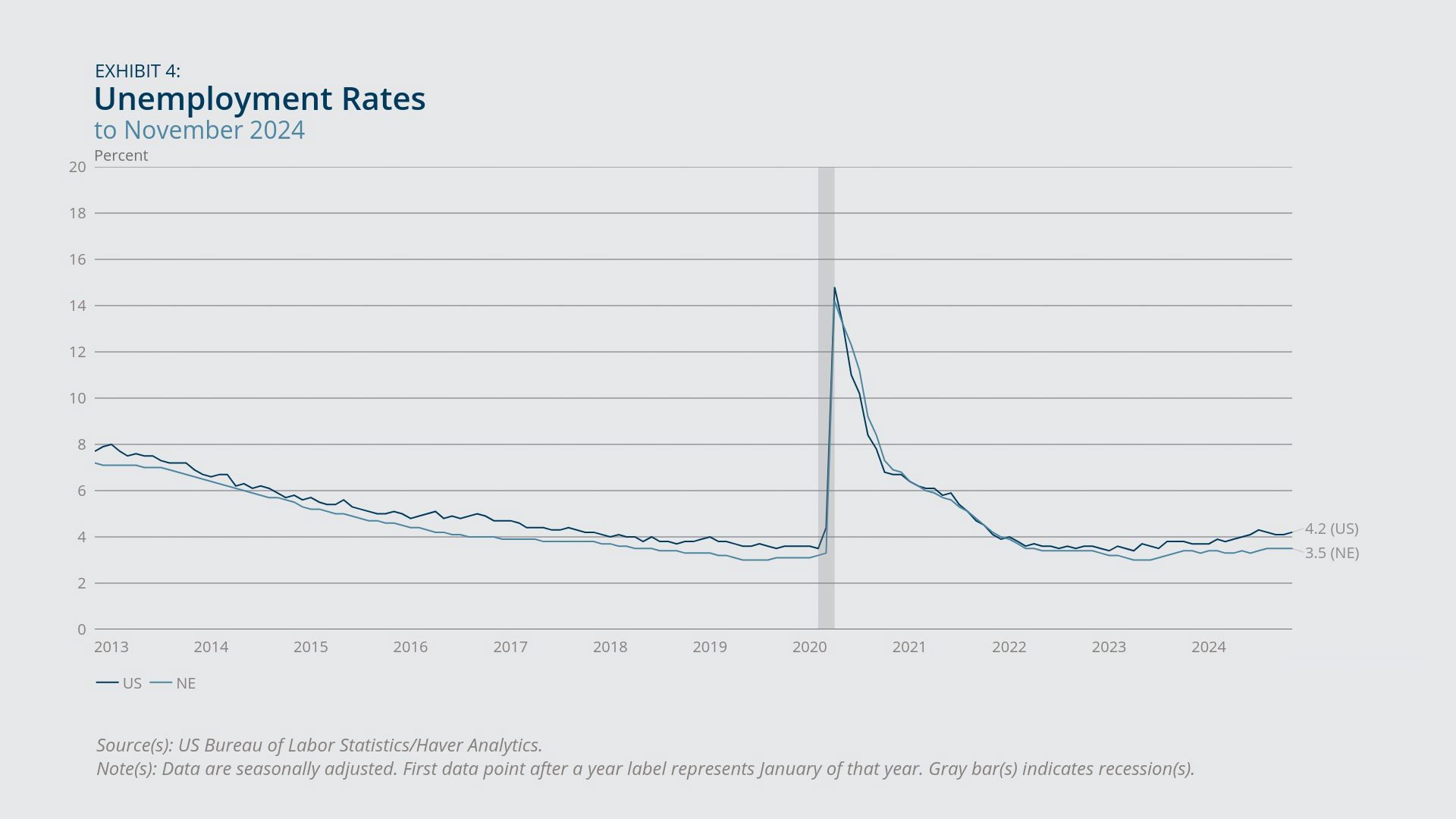

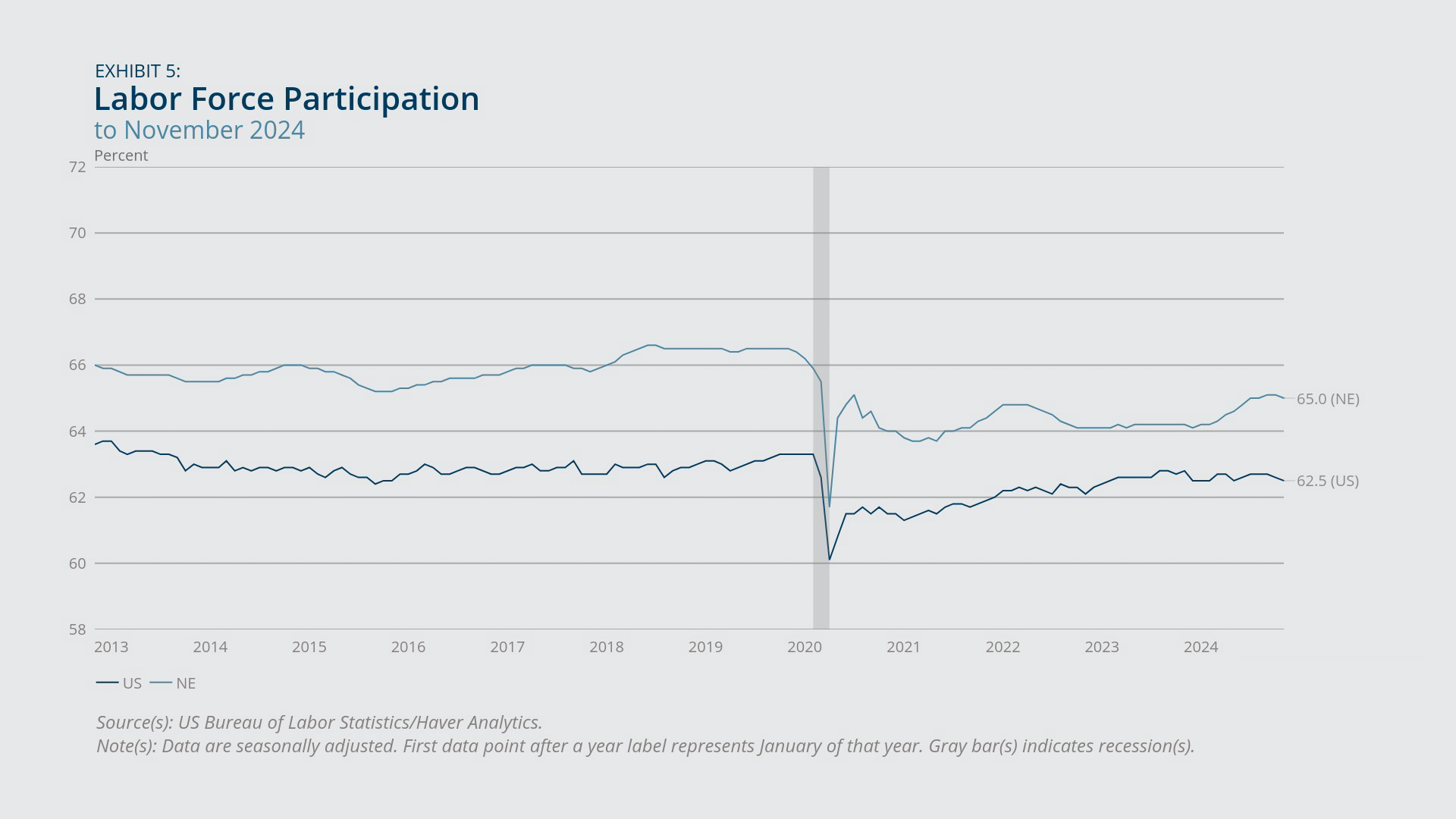

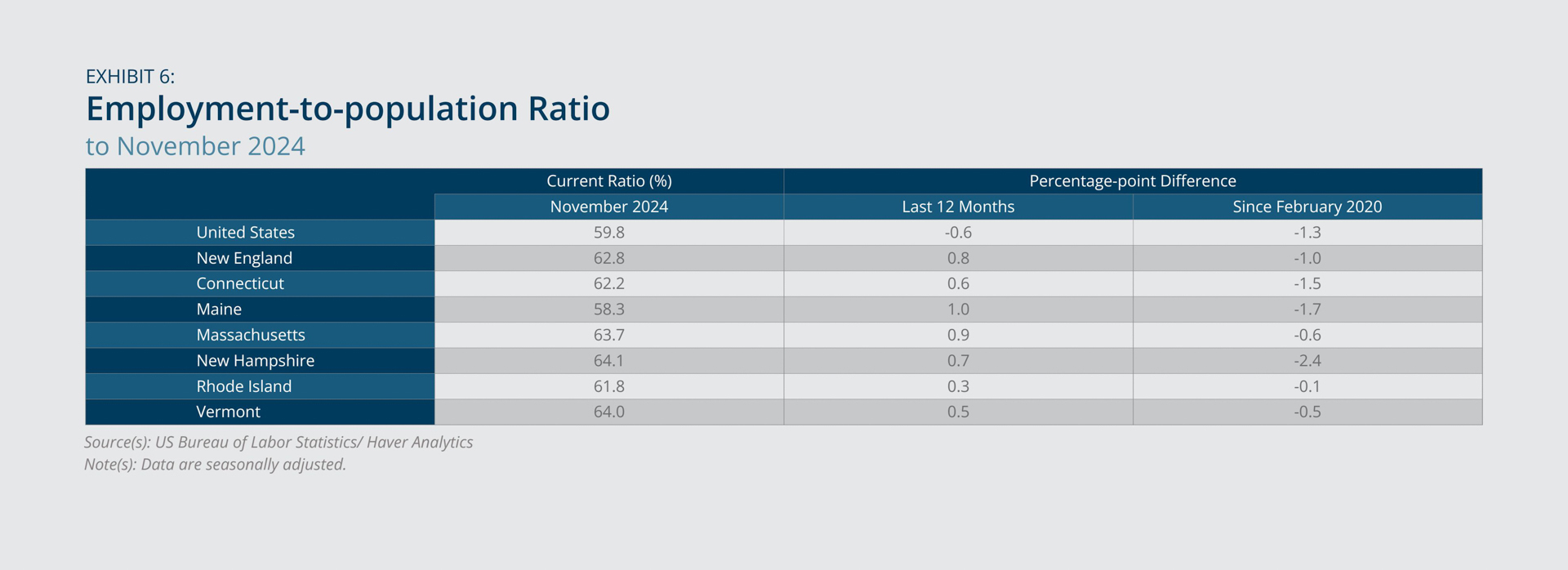

The unemployment rate stood at 3.5 percent in New England and 4.2 percent nationwide in November 2024 (Exhibit 4). The rates reflect year-over-year increases of 0.1 and 0.5 percentage point, respectively. While the national unemployment rate rose steadily from November 2023 to November 2024, the region’s rate largely remained flat. Furthermore, the regional and national labor force participation rates continued to diverge, with the New England rate increasing 0.8 percentage point and the US rate decreasing 0.3 percentage point year-over-year (Exhibit 5). As a result of the stable unemployment rate and increase in labor force participation rate, the region’s employment-to-population ratio saw a substantial 0.8 percentage point increase over the 12-month period ending in November 2024, in contrast to the 0.6 percentage point decline nationally (Exhibit 6). The increase in the employment-to-population ratio ranged from 0.3 percentage point in Rhode Island to 1.0 percentage point in Maine, highlighting the resilience of the labor market across the New England states.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Inflation

- Year-over-year inflation in New England continued to decelerate in November 2024, gradually aligning with the national rate.

- Moderation in price appreciation across key expenditure categories, including shelter, transportation, medical care, recreation, and education, contributed to the overall cooling of inflation in the month.

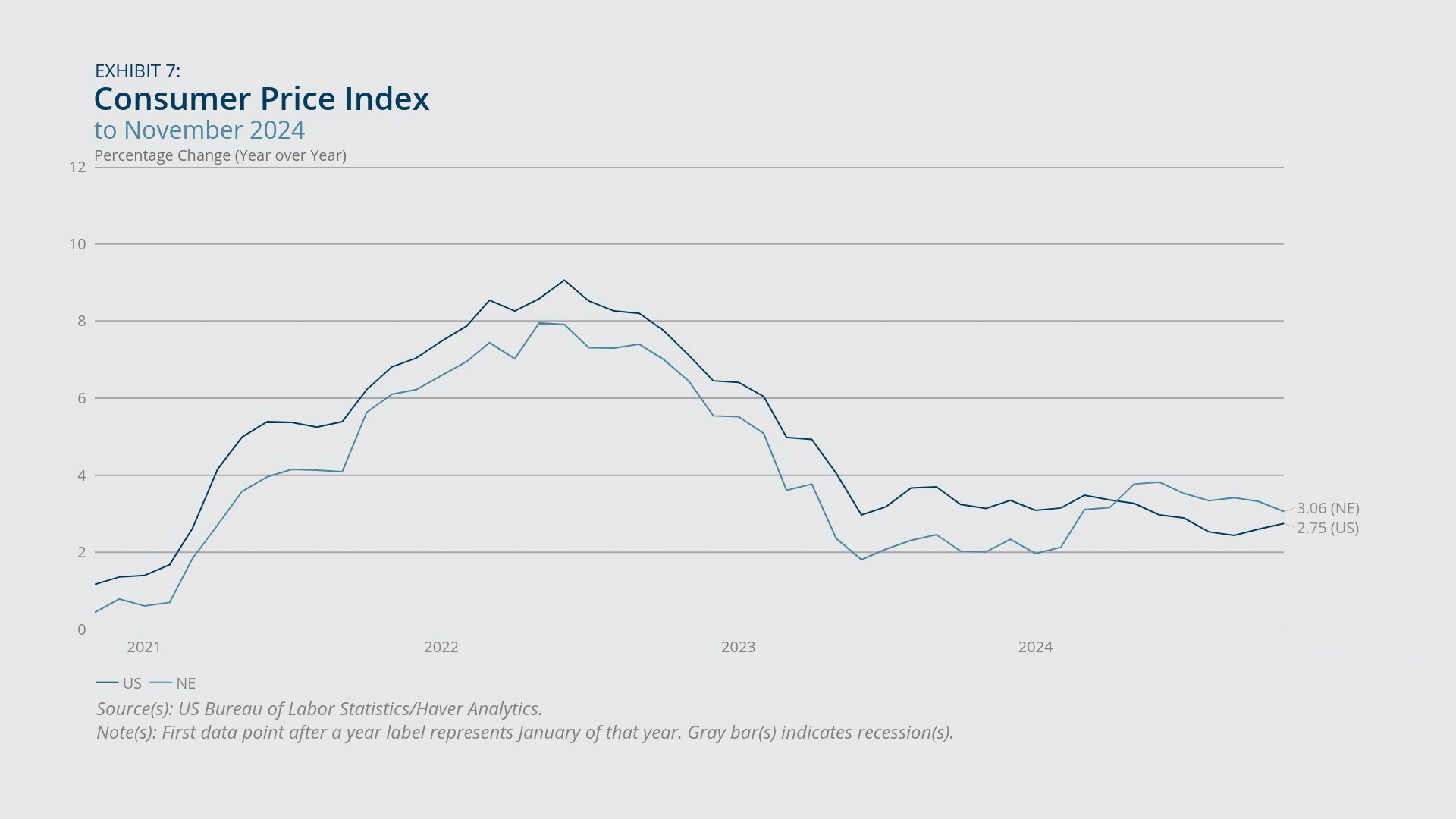

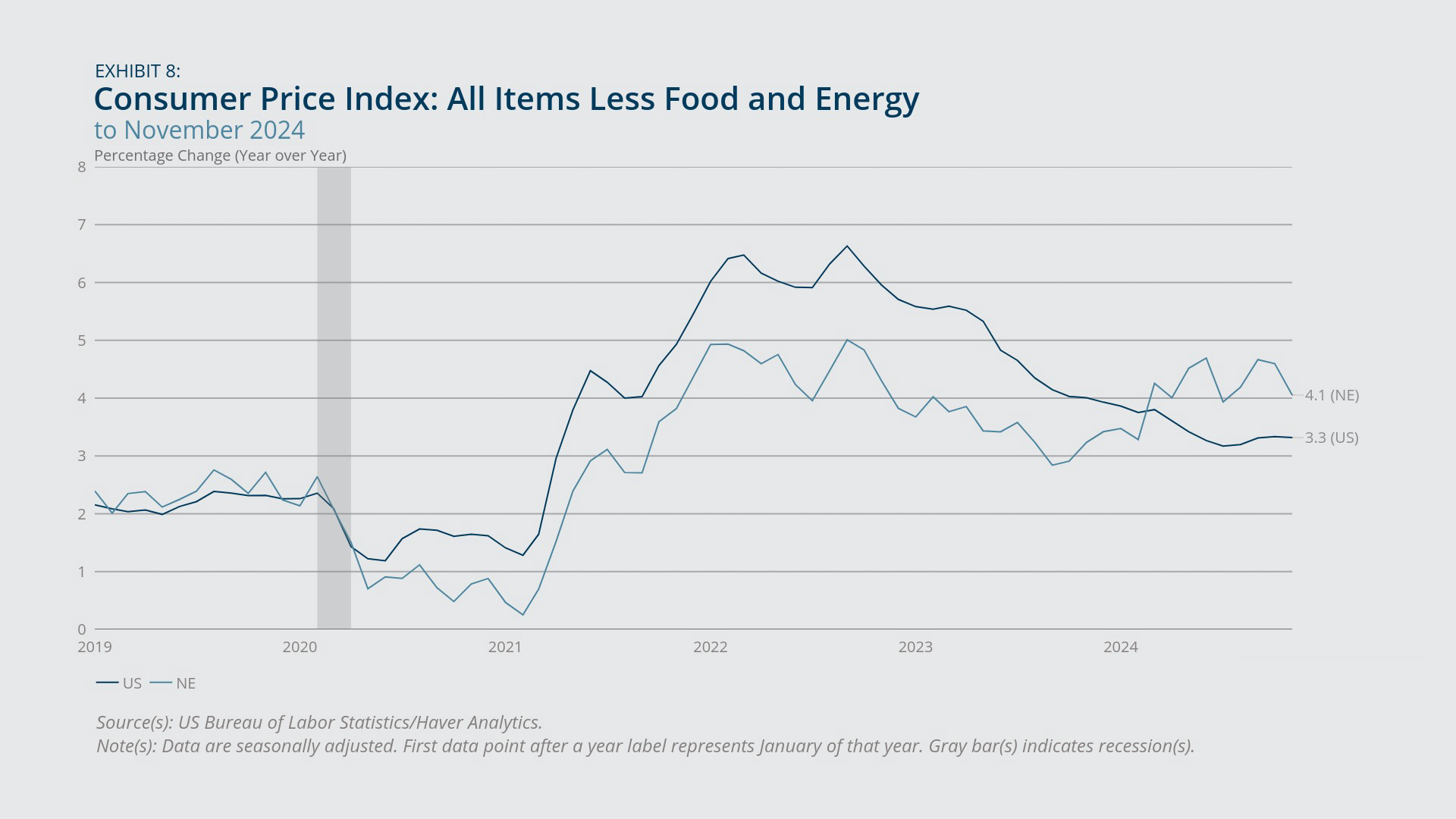

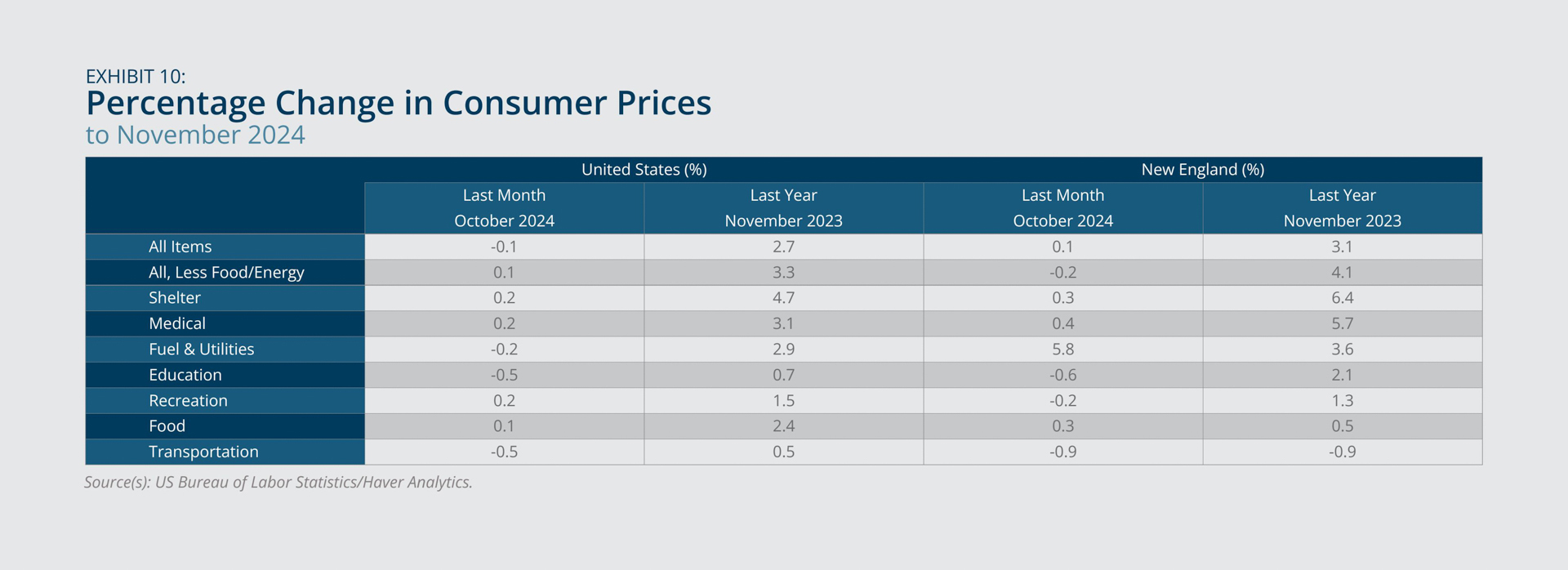

In November 2024, inflation, as measured by the year-over-year change in the Consumer Price Index for All Urban Consumers (CPI-U), was 3.1 percent in New England and 2.7 percent nationwide (Exhibit 7). The rates reflect a 0.2 percentage point decrease in the region and a 0.1 percentage point increase nationally from the preceding month. During the same period, core inflation, which excludes the more volatile food and energy expenditure components, fell 0.5 percentage point in the region (Exhibit 8). Inflation in New England had been decelerating since July 2024, gradually converging with the national rate.

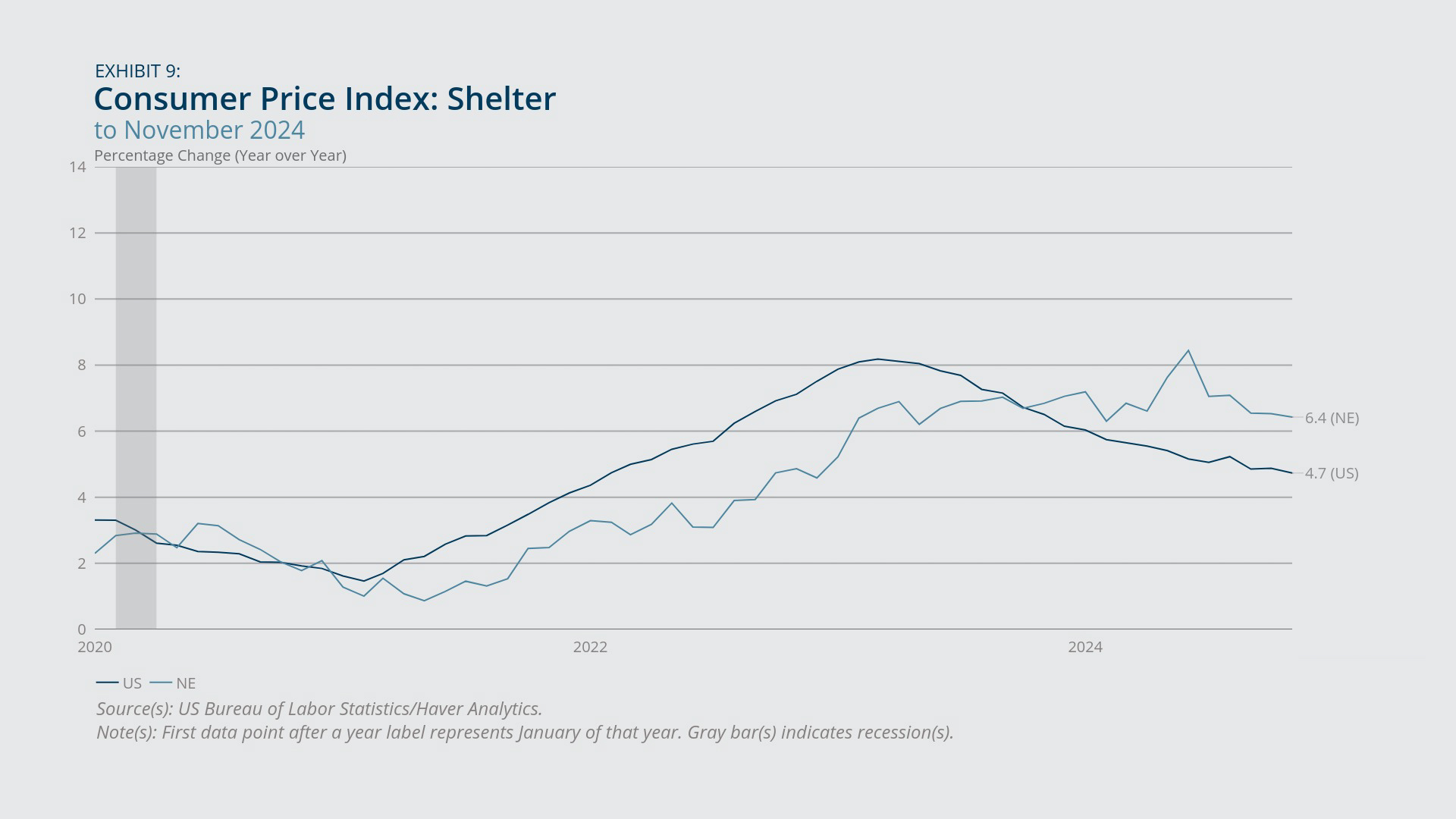

Shelter inflation remained the primary driver of the region’s core inflation, but it had softened in recent months. From October to November 2024, the year-over-year shelter inflation rate declined 0.1 percentage point to 6.4 percent, down from a peak of 8.4 percent in June 2024 (Exhibit 9). In addition to shelter inflation moderating, inflation across the transportation, medical care, recreation, and education expenditure categories slowed, contributing to the overall cooling of core inflation (exhibit 10).

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Real Estate Markets

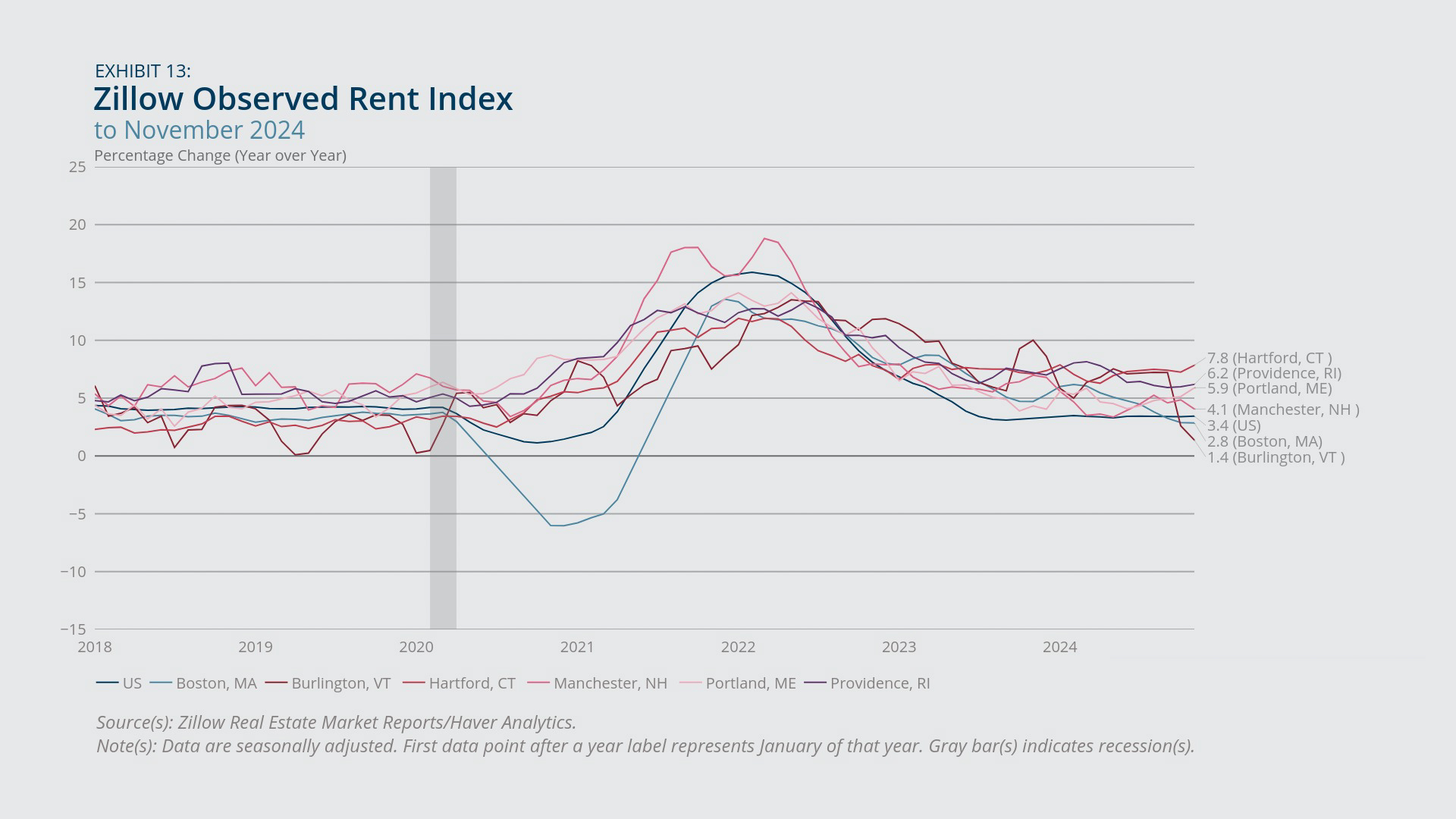

- Year-over-year house-price and rent growth in New England continued to decelerate, with Vermont, Massachusetts, Maine, and New Hampshire experiencing a more substantial slowdown compared with Connecticut and Rhode Island.

- The variation in house-price and rent growth trends reflects differential changes in population and housing demand across the region in the post-pandemic period.

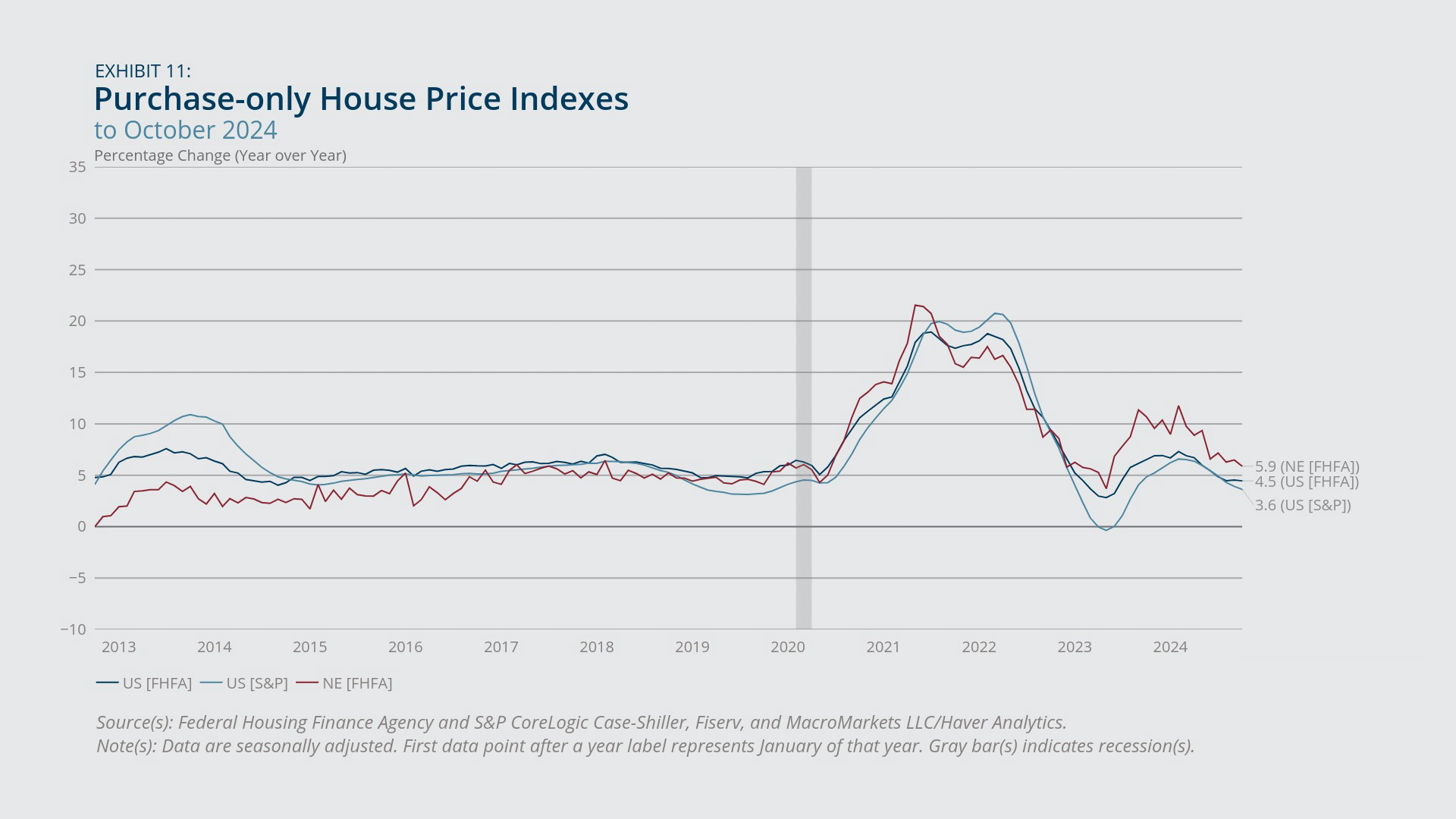

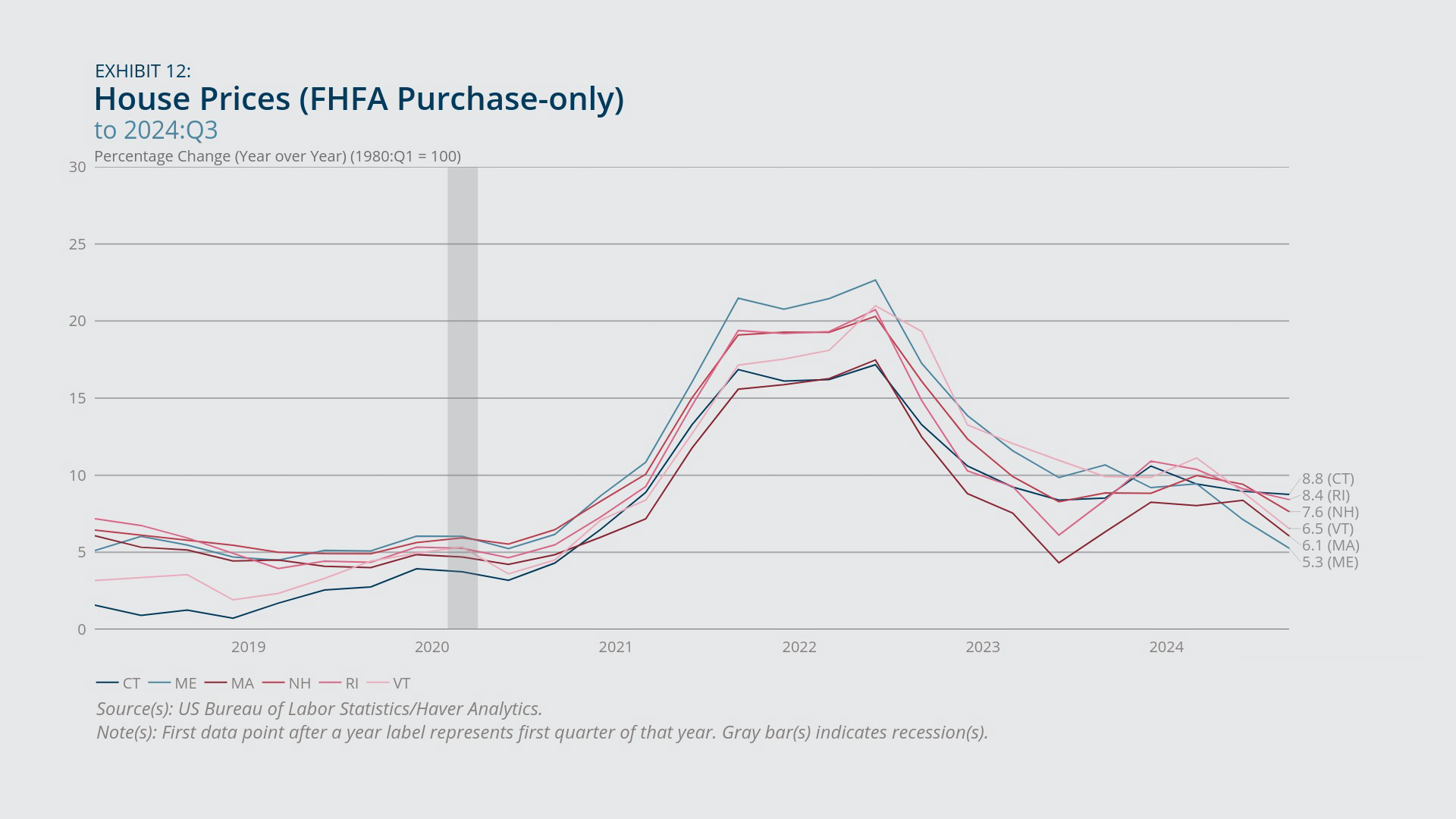

According to the Federal Housing Finance Agency (FHFA) House Price Index, year-over-year house-price growth in New England continued to decelerate after February 2024, reaching 5.9 percent in October 2024, a level comparable to the pre-pandemic growth rate in January 2020 (Exhibit 11). Among the New England states, Vermont, Massachusetts, Maine, and New Hampshire experienced a more substantial slowdown in house-price growth, while Connecticut and Rhode Island saw only a modest decline from the second to third quarter of 2024 (Exhibit 12). Consistent with this house-price growth trend, rent growth, as indicated by the year-over-year change in the Zillow Observed Rent Index, also varied across the region. As of November 2024, rent growth had decelerated and fallen to levels below the 2019 baseline in Boston, Burlington (Vermont), and Manchester, but it remained relatively elevated in Hartford and, to a lesser degree, Portland and Providence (Exhibit 13). The more persistent house-price and rent growth observed in Connecticut suggests an increase in housing demand, which aligns with the state’s population gain observed over the past two years.1

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Consumer Confidence

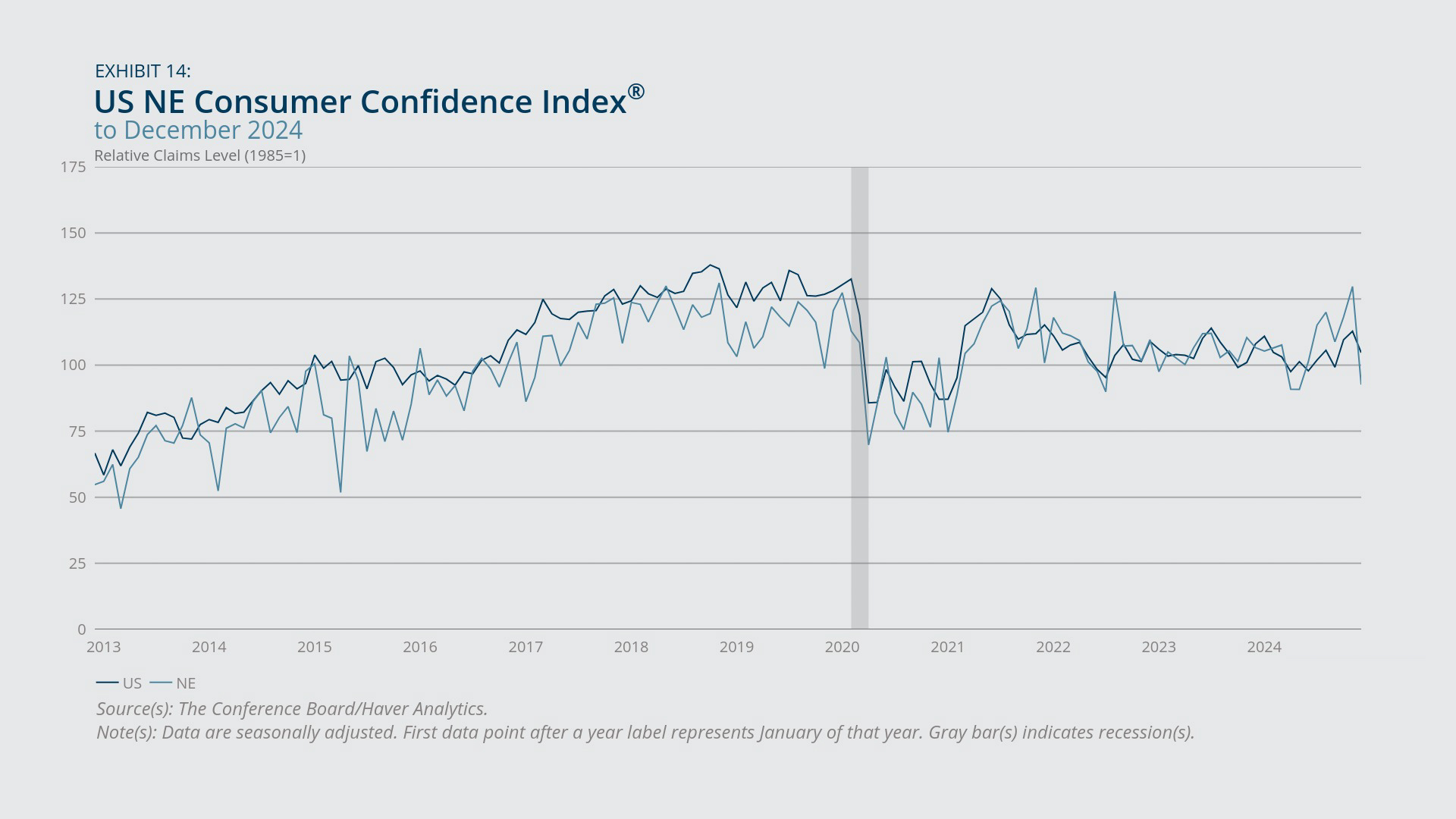

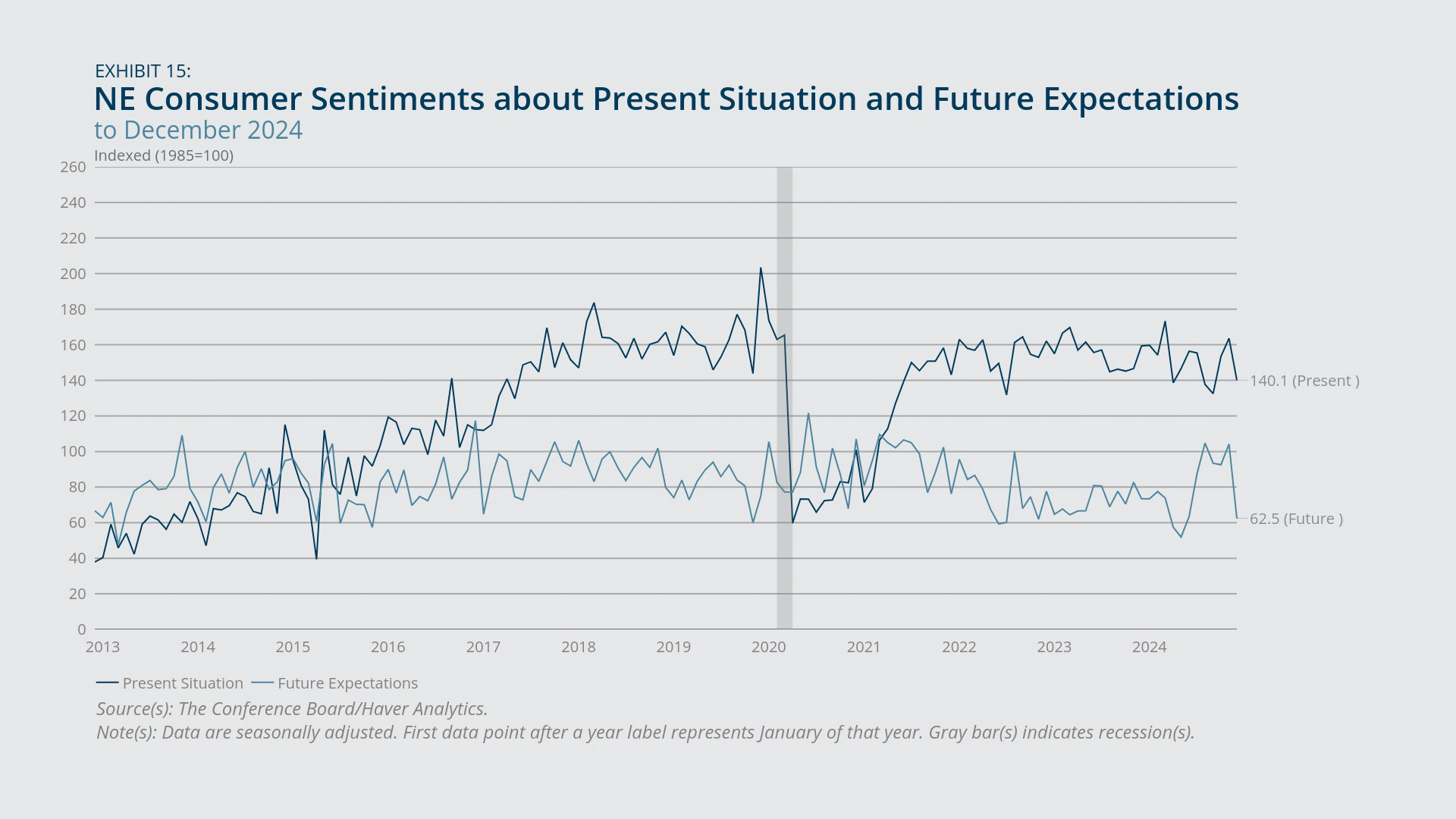

- New Englanders’ consumer confidence trended upward from May through November 2024 but softened again in December 2024, with the yearly average remaining modestly below the pre-pandemic baseline.

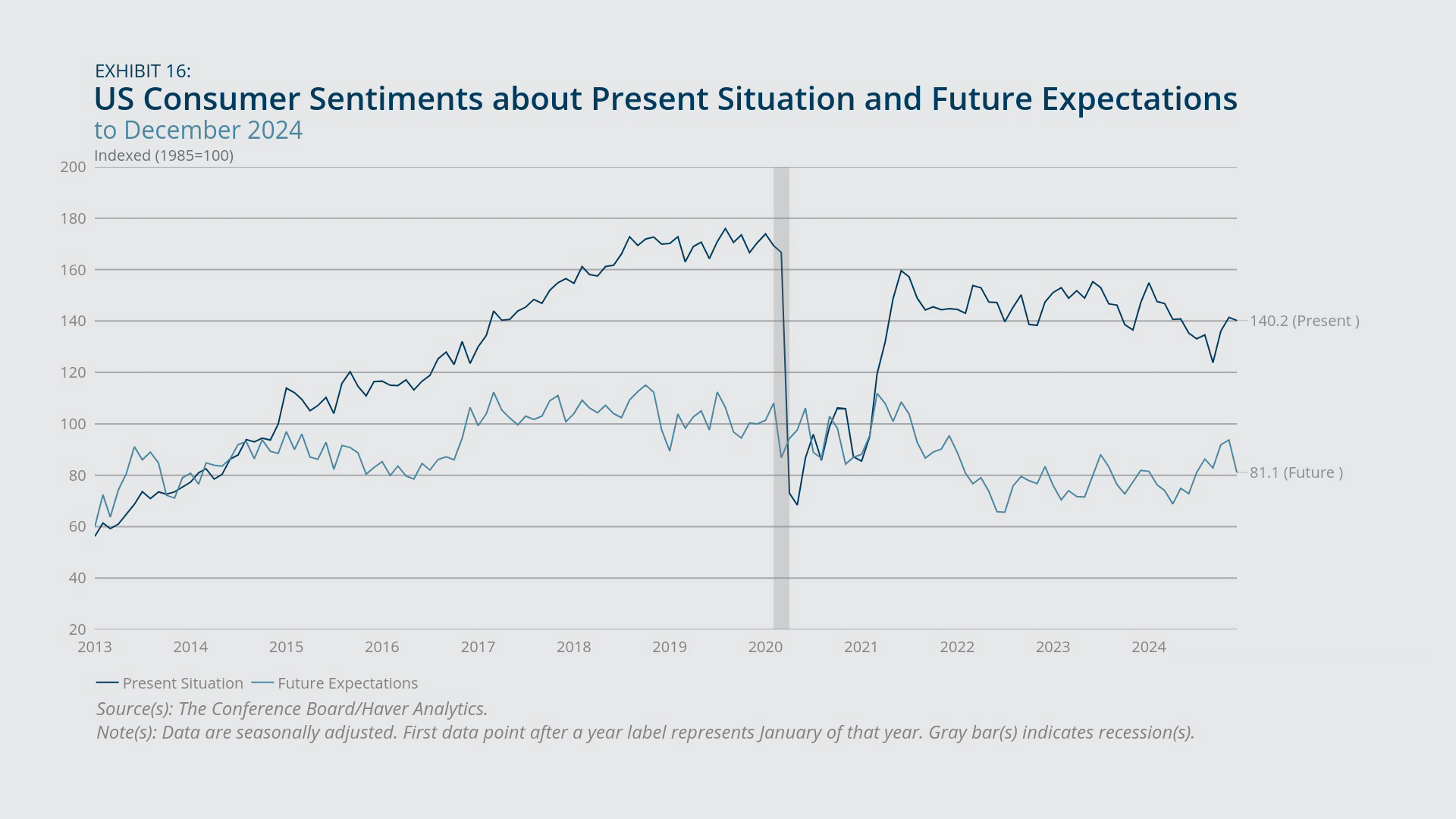

- Nationally, consumer sentiment about the present situation declined steadily from January to September 2024 before improving thereafter, while future expectations trended upward from April to November 2024, indicating concerns about current conditions but cautious optimism about the economic outlook.

New Englanders’ consumer confidence, as measured by the Conference Board’s Consumer Confidence Index, exhibited an upward trend from May through November 2024 but softened again in December 2024 (Exhibit 14). This trend was driven primarily by fluctuations in future expectations, while sentiments about the present situation remained largely stable throughout the year (Exhibit 15).

Nationally, consumer sentiments about the present situation declined steadily from January to September 2024 but improved thereafter (Exhibit 16). Conversely, US consumers’ future expectations followed an upward trajectory from April 2024 to November 2024 but weakened modestly in December 2024. As of December 2024, the national indexes for sentiments about the present situation and for future expectations remained depressed compared with the 2017–2021 period, suggesting that US consumers were cautiously optimistic about the future but continued to have reservations about the overall strength of the economy.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Endnotes

- See Cynthia Willner, “Census Bureau Releases Vintage 2024 State Population Estimates,” CT Data, December 20, 2024, https://www.ctdata.org/blog/vintage-2024-state-population-estimates; and Pinghui Wu, “Geographic Mobility Trends: New Englanders Still Aren’t Moving as Much as They Did before the Pandemic,” Federal Reserve Bank of Boston New England Public Policy Center Regional Briefs 2024–3, https://www.bostonfed.org/publications/new-england-public-policy-center-regional-briefs/2024/geographic-mobility-trends-new-englanders-still-arent-moving-as-much-as-they-did-before-the-pandemic.aspx#collapse2.

About the Authors

About the Authors

Pinghui Wu,

Federal Reserve Bank of Boston

Pinghui Wu is a senior economist with the New England Public Policy Center at the Federal Reserve Bank of Boston.

Email: Pinghui.Wu@bos.frb.org

Annie Liu,

Federal Reserve Bank of Boston

Annie Liu is a research assistant with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Kelly Jackson,

Federal Reserve Bank of Boston

Kelly Jackson is a senior data analyst in the Federal Reserve Bank of Boston Research Department.

Resources

Keywords

- Regional economy ,

- Economic Conditions ,

- New England